Wealthy Americans Are Rushing To Set

Up Tax-Free Retirement Accounts

To Lock In More Growth, Less Tax, and More Security

How can you unlock Tax-

Free Retirement?

Do you know who Ted Benna is? He founded the 401(k) along with the Revenue Act of 1978, which allowed employers to create tax-advantaged savings accounts for their employees. That’s right. 1978.

Recent, isn’t it?

Now Ted Benna has regrets. He never intended for it to be the primary mechanism for retirement income, but rather a supplement to pensions.

86% of Americans have either a 401(k) and/or an IRA, but their retirement savings are exposed to two giant threats:

Unnecessary taxes

Risk of market loss

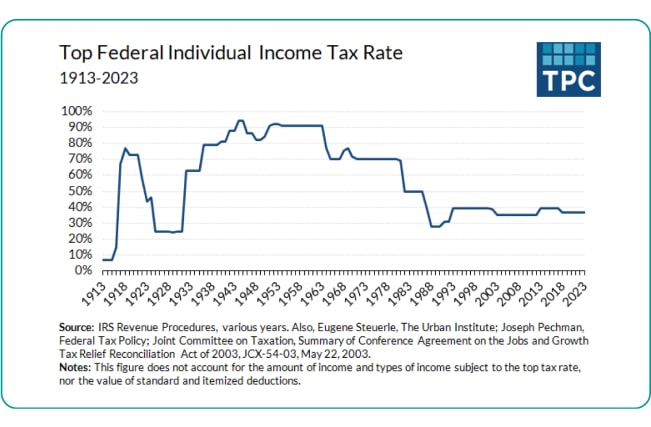

The most sophisticated investors know that taxes are one of the primary problems they must solve. Why? Because you‘ll live off after-tax dollars. Currently, taxes are at historic lows. So where do you think tax rates will be in 5, 10, or even 20 years? Likely higher…

What about the other risk? Market downturns…

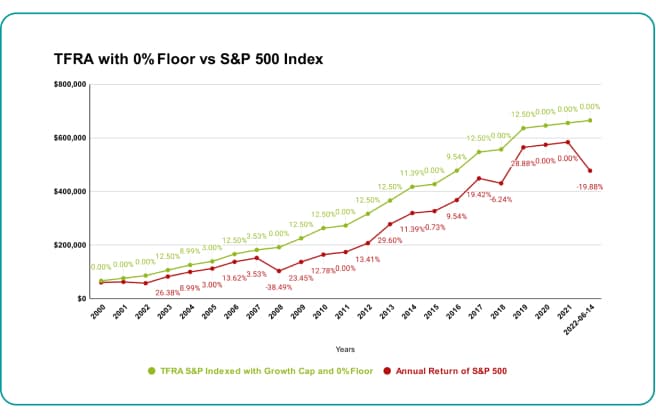

The TFRA has a 0% floor, which means your investment never goes down in value.

This is the difference between a $100K investment in 2000 with a 0% floor vs. the traditional method of investing in the stock market.

The green looks pretty appealing, doesn’t it?

Discover The Secrets To A Tax-Free Retirement During

Your Complimentary TFRA Strategy Session

In As Little As 5 Minutes, You Will Discover How To:

Remove Market

Risk

The ups and the downs of market volatility can be difficult to manage through,

but not with a TFRA,

which shelters you from

market downturns

Avoid Paying

Unnecessary Tax

Don’t pay more than your fair share of tax. Once you’ve set it up, all the money you make from it,

and take from it,

can be 100% tax-free

Keep Your

Money

Liquid

All money that you put into and made in your account stays

completely liquid

Maximize your retirement in 3 easy steps

Step 1

A TFRA Retirement Specialist will examine your current retirement

accounts and determine (down to the penny) exactly how much you’re on track to earn from your investments (401K, IRA,TSP) and Social Security in retirement.

Step 2

Your TFRA Retirement Specialist will plug your numbers into our proprietary Tax-Free Retirement App that compares your current outlook to what you could earn with a TFRA. The goal is to plainly see which option is best for your retirement goals.

Step 3

After analyzing the thousands of different investment vehicles available to you through a TFRA, your Tax-Free Retirement Specialist will work with you to determine the 1-3 best high-performing account options that significantly outperform your existing retirement accounts.

From there, we’ll help you get approved for this IRS-Approved strategy and set up your Tax-Free Retirement Account.

Customer Testimonials

Thanks to the team over at TFRA I don’t have to worry about my retirement accounts anymore.

I’ve been hearing about using life insurance as an investment vehicle so much on social media recently...so glad to have found the team at TFRA!

I never even knew how much I’d have in retirement. Now I have a plan in place too. Thanks TFRA team!

I’ve been so tired of riding the stock-market roller coaster and the constant worry. Now I’ve got a TFRA and never need to worry!

Frequently Asked Questions

How Does a TFRA compare to traditional options?

With a 401K:

❌ Your growth & principal is not guaranteed (most 401(k)s rise & fall with the market)

❌ You’re expected to shoulder all the risk

❌ You have limited/no access to professional advisors (or you’re not seeing a return on your costly advisors’ fees)

❌ You and your spouse aren’t guaranteed a dime of life-long income

With a Roth IRA:

✅ You don’t pay taxes on growth, but…

❌ You can only deposit $6,000 /yr

❌ Growth & principal isn’t guaranteed – like most 401(k)s

❌ Not liquid (same 10% early withdrawal penalty)

With a Tax-Free TFRA:

✅ You never pay taxes on growth, Ever. ( This is 100% legal if your TFRA is set up to be compliant with current IRS tax-code.)

✅ You can deposit as much as you want. (No contribution limits – every cent in grows tax-free)

✅ You never report income to the IRS, Ever. (The IRS doesn’t classify “income” as “income” inside this kind of account)

✅ Your interest rate can be guaranteed. (Your money grows at the same yearly rate as when you opened your account— even if the market crashes)

✅ Your money can be liquid. (Your account growth and value— can be accessed in any amount—at any time—without penalty)

Who else has used this?

Walt Disney

He used a TFRA to fund Disneyland.

Ray Kroc

The founder of McDonald’s also used a TFRA to keep his business alive during the early years.

J.C. Penney

He used his TFRA to meet his payroll during the Great Depression.

Jim Harbaugh

The most famous coach in college sports will be able to take out $1.4 million a year in Tax-Free Income when he retires because of his TFRA.

And many many more (including Presidents and many major companies in the U.S.)…

If a TFRA is so great, why hasn’t my financial advisor ever told me about this?

REASON 1: Most financial advisors don’t know Tax-Free Retirement Accounts (TFRA) exist – nor how to structure one that maintains a tax-advantaged status for the account holder.

REASON 2: Most financial advisors only recommend the financial vehicles their company tells them to recommend.

Who is a TFRA for?

Are you a high-income earner looking for additional retirement savings vehicles beyond the traditional?

Are you a business owner?

Are you looking for tax-advantaged growth and to be able to take tax-free withdrawals?

Do you have an old or underperforming 401K, IRA, TSP?

Do you want to participate in the growth of the stock market but don’t want the downside?

Or maybe…

You keep crunching the numbers and pushing your retirement dreams back year by year?

Yes? Then a TFRA could be right for you!

But to know for sure, you need to click below and drop us a note.

Do You Qualify For A Tax-Free Retirement

Account?

By pre-qualifying, you are not committing to anything. This form simply provides our Tax-Free Retirement Specialists the information they need to diagnose your retirement outlook and provide the best solution for you to access the maximum amount of earnings.